How wealthy people save money for retirement?

Discover how wealthy people save money for retirement - check out our blog post for valuable tips and insights!

One may be concerned about the potential of financial depletion during retirement or a lack of knowledge in wealth management measures that provide steady income while minimizing tax liabilities. Although it may appear difficult, saving for retirement often necessitates consistency and a long-term outlook on personal finance. It is not difficult to live an enjoyable retirement. With some help, you can devise a plan to save and invest your way there.

Whether you are approaching retirement in a few years or are already living a luxurious lifestyle, it is critical to have a well-defined strategy to monitor and adjust as needed. Indeed, many of the strategies that wealthy persons use to plan for their retirement and personal finances are available to people of all income levels.

These are some of the wealthy's most effective retirement planning tactics. While not everyone follows them, they are usually easy to find.

What benefit does retirement planning provide for the wealthy?

One frequent notion among wealthy persons is that meeting with a financial counselor about their objectives is prudent. A financial advisor can offer the assistance, advice, and solutions required to reach one's goals. However, let us start by discussing why you need retirement savings programs.

Preparing for retirement allows you to follow your financial goals without worrying about insufficient money. Simply put your approach to certain parts of high-net-worth financial planning may differ slightly from that of a neighbor, close friend, or colleague. If you have a high net worth, you will have specific needs. Individualizing a retirement savings plan is the most effective way to meet long-term goals.

Because of your desire to explore the world, you may wind up paying more than someone who has no specific travel goals. Alternatively, you may already have a medical problem and are dealing with medical bills that require more complete medical coverage, but at a larger cost.

Because individuals have different amounts of cash, retirement planning techniques must be tailored to your specific needs.

In addition to their employer retirement plan, the wealthy's high-net-worth retirement plan includes the following important strategies:

Which effective retirement planning techniques do wealthy people employ?

1. Establish retirement savings targets-

If the plan's goal is to maintain your current lifestyle until you reach full retirement age, you must transform it into expenditure targets. Not settling on retirement savings goals is a major pre-retirement mistake that you must avoid.

If you already keep track of your costs, this stage will go much faster. If not, consider how much you regularly pay per month.

The cost of food, power, housing, insurance, taxes, and other requirements must all be considered. However, keep in mind that you may have to pay for "non-essentials" like weekend trips, movie or sporting event tickets, and gifts for loved ones.

It would be preferable if you did not begin by researching methods to save expenditures in this case. It may proceed to that section if necessary.

2. Diversify Your Investment Portfolio-

Investing includes risk. On the other hand, diversifying one's financial portfolio is an excellent investment strategy for wealthy individuals looking to build a safe retirement. While wealth provides a cushion, it is critical not to rely on a single asset class.

Eric Lam, Founder of Exploding Ideas, shared his investment advice: "By spreading investments across stocks, bonds, mutual funds, real estate, and other assets, you can reduce risk and enhance long-term stability. Diversification helps ensure that even in uncertain economic climates, your retirement nest egg remains robust and capable of supporting your desired lifestyle.

3. Commence projecting cash flows and include the required inflation adjustments-

After calculating your annual budget and factoring in inflation, you must estimate how much money you will need in the future.

In the past, inflation has often averaged 2.5% every year, but as you are aware, things aren't quite right currently. That's a good place to start, but you may need to alter depending on what you spend the majority of your money on.

4. Contribute to Low-Cost Index Funds-

Eric Novinson, Founder of This Is Accounting Automation, suggests: "One effective strategy to plan for retirement is to make regular contributions to a low-cost index fund. This can be done at any wealth level if you have the funds to invest, but it works just as well if you are affluent.

Alternative investments are frequently high-risk, and even if you are qualified to engage in them, they may not be the most secure option. Many rich investors in financial independence forums still prefer to invest in index funds, despite having access to other options.

5. Use the money for expansion-

Rich people invest their money to increase their wealth. Living below one's means is an effective way to save money.

In general, affluent individuals do not merely store their money. Their money is invested in growth-oriented products, and they usually use tax-advantaged "wrappers" to avoid paying taxes on capital gains. They are constantly looking for new methods to work, gain money, and advance.

Rich people do not generally look for the next big stock. Investing for growth can include regularly adding funds to a diverse portfolio. This form of investment grows gradually, rather than all at once.

6. Implement Tech-Based Investment-

A viable retirement approach for wealthy persons like myself may be to execute "tech-based investment." The idea is to channel a percentage of money into our company's technological advancements—AI, machine learning, data analytics, or blockchain. It not only gives us a competitive advantage, but it also has the ability to increase our worth, providing higher profits in the long run.

Abid Salahi, Co-Founder and CEO of FinlyWealth, stated, "As a way to keep up with rapid technological innovation and secure our retirement future, it's like hitting two birds with one stone."

7. Invest in Metro Rental Properties-

Beyond diversification, brick-and-mortar assets provide inflation-hedged income that outperforms the volatility inherent in stocks and bonds.

Jonathan Ayala, Founder of Hudson Condos, elaborated: "For the premium segment I service, rental property in attractive metro areas ranks first on my suggestion list. Professional property management ensures regular tenant occupancy and income flow with minimal effort. Expect 8-12% yearly returns, depending on area dynamics."

Self-directed IRAs provide even bigger tax benefits when reinvesting in additional property acquisitions. Tools such as Delaware Statutory Trusts provide access to big institutional assets with fractional ownership. The trick is to deal with professional advisors who understand real estate complexities, such as managing 1031 exchanges and estate planning with property assets.

8. Examine how much you have contributed-

The most obvious way to see growth in your 401(k) is to increase your annual payments. If you can get as close to the annual contribution limit as feasible, your money will have more opportunities to grow tax-free. Assume you are now unable to increase your contribution rate. If so, you might want to consider doing it annually in smaller amounts, such as 1% to 2%.

Ideally, you should be making the most money by the time you reach 50 and be able to pay the full amount each year to your 401(k). You can make catch-up payments up to the annual cap to save even more money.

Source: investopedia.com

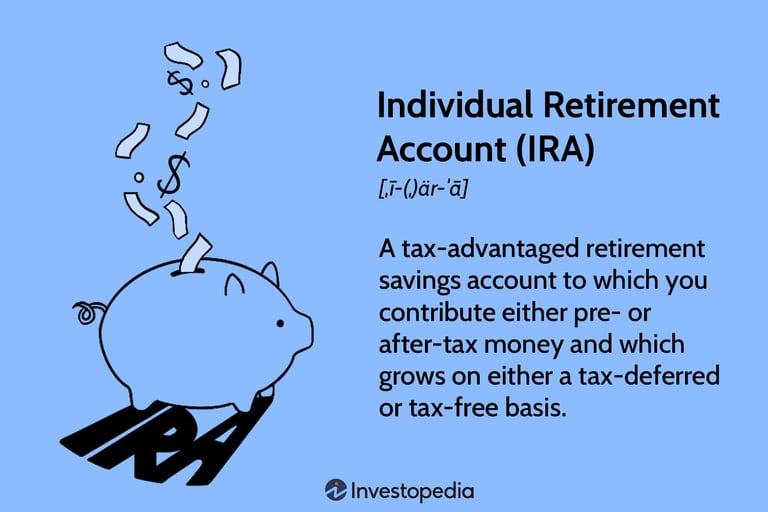

9. Lock in High-Rate IRAs-

Investing in IRAs is a sensible long-term move. Annuities and IRA rates have recently reached a 10-year high. By locking them in for a few years, you can generate enough money to support yourself. Tammy Sons, CEO of TN Nursery, stated, "This was sound advice; I wish I had waited until now to act, but we did not."

Source: money.com

10. Select the Roth conversion-

When people retire, they can make qualified withdrawals from Roth funds without paying taxes. Wealthy retirees who open this tax-free savings account will have greater autonomy, choice, and flexibility in their later years.

However, putting money in a Roth account is not always the best decision. Most people create tax-deferred accounts to save money. When they withdraw money, the IRS taxes it at their standard income tax rates. If your tax rate is high when you retire, you may end up owing more than you would like.

Contributing to both after-tax and tax-deferred accounts gives you additional alternatives when it comes to withdrawing money in retirement. Individuals with high salaries, however, are generally unable to contribute directly to Roth IRAs due to IRS-imposed limits.

One way to lawfully avoid this restriction is to "convert" monies from a regular account to a Roth account. Individuals with considerable tax savings and high incomes or net worth may benefit from converting their standard IRAs to Roth IRAs.

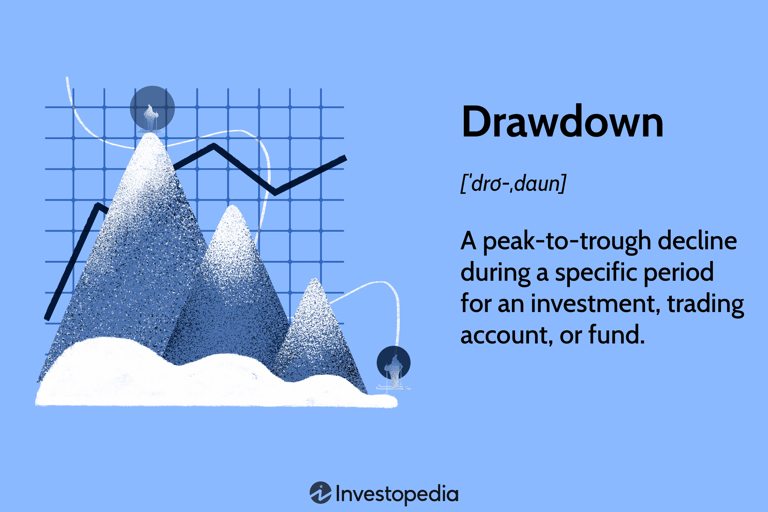

11. Establish a strategy for account drawdown-

A withdrawal strategy is more than just deciding how much money to withdraw from your retirement accounts. People typically withdraw approximately 4% of their savings in the first year; after that, they increase their withdrawals in line with inflation. However, your retirement approach should not follow a set schedule.

A planned withdrawal strategy determines how and how much retirement money should be dispersed from each account. It is determined by your income criteria, tax bracket, source of funds, and other factors. For example, withdrawals from a Roth IRA are not taxed, whereas withdrawals from a standard IRA are.

Source: investopedia.com

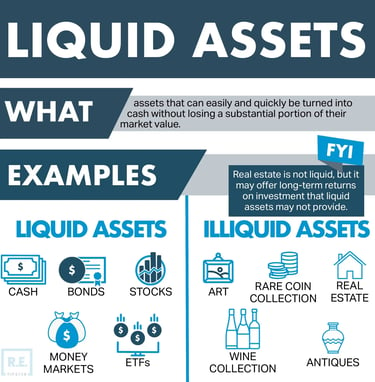

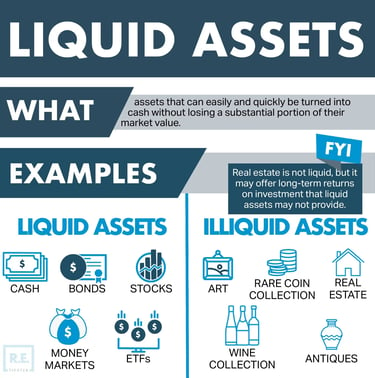

12. Verify if you have enough liquid assets-

Rich people routinely analyze their cash flow needs when formulating retirement plans. They make sure they have enough liquid money on hand. It inhibits them from selling assets to meet urgent funding needs.

Wealthy individuals often have a large amount of cash on hand, which they can use to invest in real estate, high-growth private equity, and other slow-growing assets. It means that the funds cannot be immediately turned into cash until a liquidity event happens, which can take a long time.

Aside from that, they invest in highly liquid assets. However, people who do not yet have adequate emergency funds should avoid investing in very illiquid securities.

Source: retipster.com

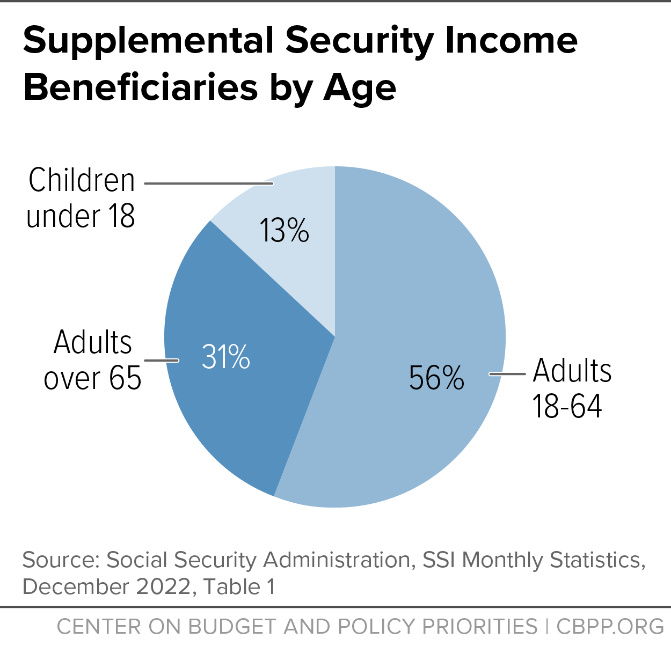

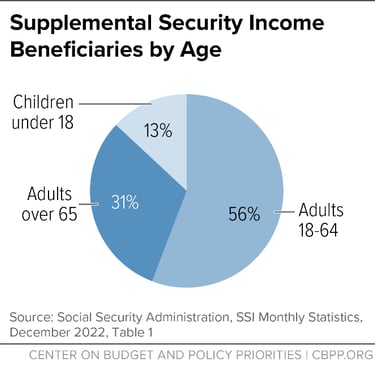

13. Establish a strategy for obtaining social security income-

Your Social Security benefits are an important part of your retirement income strategy since they provide a fixed income stream. It is an important benefit that you should take advantage of, even if it does not make up the majority of your retirement income. You can rely on Social Security to give you a steady income that is unaffected by inflation, market fluctuations, or expiration.

Source: cbpp.org

14. Include health care in your retirement plans-

Managing your medical expenses and health is an important component of a retirement strategy. Fidelity estimates that healthcare costs account for 15% of a retiree's take-home pay. You must account for long-term care, Medicare payments, and out-of-pocket spending. Regardless of your viewpoint, you will need to spend a large amount of money on health care throughout retirement.

Medicare will be the key component of your healthcare plan. As with Social Security, you must ensure that your Medicare plan is enough. Never follow a set of standards or a planned method solely because your friend did. Examine the numerous coverage alternatives while taking into account your needs, financial status, and lifestyle.

Another alternative is to contribute some of your funds to a health savings account (HSA). If you have a high-deductible health plan, you can contribute to these tax-advantaged accounts to save money.

Roy Lau, co-founder and CEO of 28 Mortgage, explained: "By planning for long-term care, wealthy individuals ensure a secure future while preserving their wealth. For example, a wealthy individual who develops a chronic illness requiring extensive care may otherwise deplete their assets quickly without proper insurance coverage. By having a long-term care plan in place, they can access quality care without jeopardizing their financial security."

15. Think about your taxes

Investing for growth often has tax implications. When planning for retirement, wealthy persons usually seek ways to lower their tax liabilities by boosting tax deductions. They accomplish this by structuring their investment accounts to pay as little tax as feasible. If you profit from a taxable retirement account, you may be required to pay taxes on an annual basis. This is not the same as holding dividend-free stocks to avoid paying taxes.

Because of the contribution limits and their high net worth, wealthy investors commonly invest in tax-advantaged retirement savings accounts such as 401ks and standard IRAs. This means that you have a substantial quantity of savings in brokerage or taxable accounts.

Nonetheless, you can manage the investment plan to generate short-term gains while meeting your financial goals, or you can invest in securities that will help you save taxes, such as tax-free local bonds.

Wealthy individuals may direct extra funds from productive investments to assets that will appreciate without raising their taxable income. This allows them to invest their money more tax-efficiently. They can use their excess assets to build an accumulation portfolio, which means no money leaves them because they no longer require new finances. Compared to a distribution portfolio, where money is continually taken from the portfolio, this is more tax-efficient.

16. Create a Trust or draft a Will-

Wealthy people think about more than just increasing their retirement savings or investments. They also consider what will happen to their belongings after they pass away. Planning your wealth can help with this. Estate planning is the official process of establishing how your assets will be dispersed after death and is one of the most effective retirement planning methods.

If you have a lot of money, you'll probably need more than just a will. By forming a trust, you can lower the amount of taxes your estate is required to pay, protect your assets from creditors, and preserve control over how your assets are dispersed to beneficiaries. Furthermore, a trust may protect your heirs from probate. The length of this process, as well as the legal fees associated with it, may reduce an individual's inheritance.

It will depend on your needs and the level of trust you wish to develop. Trusts take many shapes, but they all require a manager you can trust. As the grantor of a revocable trust, you can also serve as its trustee. If you create an irrevocable trust, you must choose another individual as trustee. Beneficiaries, or the people who will receive money or other assets from the trust, must also be identified in any trust.

17. Seek Professional Financial Advice-

Seeking professional guidance from financial counselors and investment managers before starting retirement planning. This is because the advice they provide will be specialized and geared to your specific objectives. To arrange your retirement investments, visit a tax planner, a certified financial planner, or a fiduciary financial advisor.