What is fractional reserve banking? How does it work?

Learn about fractional reserve banking and how it works in our easy-to-understand blog post - broaden your financial understanding and read today!

3/26/20246 min read

What Is Fractional Reserve Banking?

Source: Investopedia.com

Fractional reserve banking is a system in which only a portion of bank deposits must be available for withdrawal. Banks simply need to have a certain amount of cash on hand and can provide loans using the funds you deposit. Fractional reserves help to boost the economy by freeing up cash for lending. Today, most economies' financial systems employ fractional reserve banking.

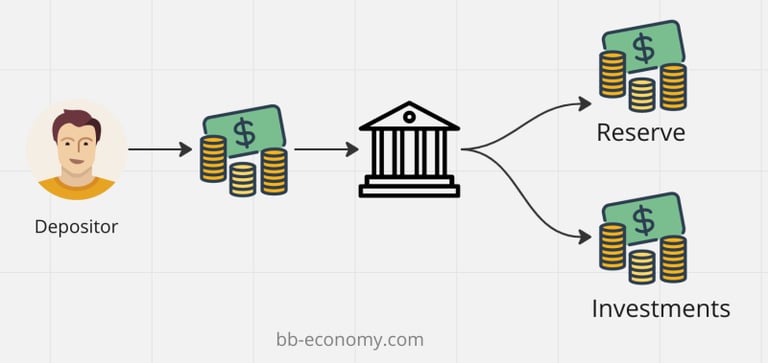

When you open an account with a bank, you agree in the contract to enable the bank to use a portion of your deposits as loans to other bank customers. This does not imply that you do not have access to the money you deposited; it simply means that if you want to remove more than the proportion a bank has on hand, such as the entire sum, from the account, the bank will need to access funds from elsewhere to give you your balance.

When you put money in your savings account, your bank can utilize the amount you specify as capital to fund loans and compensate you for using your money. For example, suppose you put $2,000 in a savings account. Savings accounts pay interest—usually between 0.5% and 2%—so you get an interest payment on your money, and the bank can use some of it for a loan. In turn, the bank may seek to utilize 80% of your money to make loans to other clients.

The Federal Reserve sets interest rates. They are based on economic conditions and how it determine how to best accomplish its twin goals of maximum employment and price stability. If a bank needs money to support loans, withdrawals, debt repayment, or other commitments, it can borrow from other banks and pay interest. As a last resort, the Federal Reserve maintains a service called the discount window, where it lends money to banks at a higher interest rate than they charge between themselves. This encourages banks to seek funds from one another rather than the Fed.

The Federal Reserve Board of Governors establishes the Federal Reserve target rate range, which governs interest rates charged between financial institutions. The average interest rate that banks charge each other is known as the effective Federal Funds Rate.

Source: bb-economy.com

Understanding Fractional Reserve Banking

Fractional Reserve Banking Process

The fractional reserve banking method creates money that is put into the economy. When you deposit $2,000, your bank may lend 90% of it to other customers, as well as 90% from the accounts of another five consumers. This generates sufficient capital to fund $9,000 in loans.

Your balance remains $2,000, and the consumers from whom the bank borrowed also have their balances unchanged. If all five customers' account balances are $2,000, it will look like this:

You and four other clients have $2,000 in savings accounts with a 1% annual return.

If the bank can lend 90% of its deposits, the available capital is $9,000 (90% of $10,000).

A sixth consumer requests for a $1,000 loan.

The bank borrows $1,000, or 10% of each of the five accounts.

Each account still has a $2,000 amount ($10,000 total across all five).

The bank simply manufactured $1,000 and loaned it to the borrower at 5% per year.

You receive 1% interest payments every year on your $2,000, and the bank keeps the 4% difference as profit.

Source: researchgate.net

History of Fractional Reserve Banking

Fractional reserve banking is said to have originated during the exchange of gold and silver. Goldsmiths would issue promissory notes, which were eventually employed as a medium of exchange. The smiths utilized the deposited gold to make interest-bearing loans, therefore establishing fractional banking.

In the United States, the National Bank Act was created in 1863, requiring banks to keep reserves on hand to prevent depositor funds from being invested in dangerous assets.

The Federal Reserve Act of 1913 established the Federal Reserve System, which we now refer to collectively. Banks were required to maintain reserve balances with the Federal Reserve Banks.

During this time, banks with less than $16.3 million in assets were not required to maintain reserves. Banks with less than $124.2 million in assets but more than $16.3 million were required to maintain a 3% reserve, while banks with more than $124.2 million in assets were required to maintain a 10% reserve.

On March 26, 2020, the 10% and 3% necessary reserve ratios against net transaction deposits were cut to 0% for all banks, thus eliminating reserve requirements.

It was replaced with Interest on Reserve Balances (IORB), which is interest paid on reserves held by banks as an incentive rather than a necessity.

Source: cobdencentre.org

Fractional Reserve Banking vs. Other Types of Banking

Most countries now utilize fractional reserve banking since 100% reserve banking is not possible. Furthermore, a system that compels banks to hold 100% of deposits cannot generate new money without depreciating the currency. To provide loans, banks would need a considerable amount of cash.

This would significantly restrict growth in both developing and established economies because banks would be unable to offer debt to businesses and people who rely on it for major purchases and investments.

A system based on precious metals, such as gold, is similarly susceptible to this problem. If a specific amount of gold must represent a given quantity of a country's currency, the country's economic potential is limited because gold has a finite supply. To fulfill the rising demand for capital, the currency's value would steadily decrease. Fractional reserve banking enables a country to increase its money supply in response to economic growth.

Advantages and Disadvantages of Fractional Reserve Banking

Pro Explained

Banks do not need to maintain large quantities of capital. Because banks use deposits that customers leave in their accounts, fractional reserve banking frees up capital for the economy. This promotes economic progress by keeping funds flowing.

Banks promote the economy via lending. The economy needs capital to grow. Banks address this requirement by lending to businesses and consumers using reserve cash. Fractional reserve banking, for example, allows for mortgages, vehicle loans, and other types of loans. Without it, most consumers would be unable to afford housing and other needs of contemporary life.

Allows for regulation: Reserve ratios can be used by central banks to regulate the economy at the macroeconomic level. Increasing reserve requirements limit lending, slowing the economy. Decreased reserve requirements increase lending, which expands the economy. Although the Federal Reserve rarely uses this instrument, other central banks, most notably the People's Bank of China, do.

Cons Explained

Consumer panic can lead to large withdrawals and a lack of capital: When consumers, investors, and businesses become concerned about economic conditions, they rush to their banks to withdraw everything they can to avoid additional losses. This is known as a bank run, and a fractional reserve system prevents people from withdrawing their capital because the banks do not physically have it.

Too much lending can lead to economic overheating: when the economy expands, it grows. During expansionary periods, consumers spend more and banks lend more. When additional money is created through loans, demand can skyrocket, driving up prices. Producers increase production to fulfill demand. This can lead to the economy overheating and growing too quickly.

Pros

Banks do not need to hold large sums of capital.

Banks stimulate the economy by lending.

Provides for macroeconomic regulation.

Cons

Consumer fear can result in massive withdrawals and a lack of capital.

Excessive lending can cause the economy to overheat.

Source: academy.binance.com